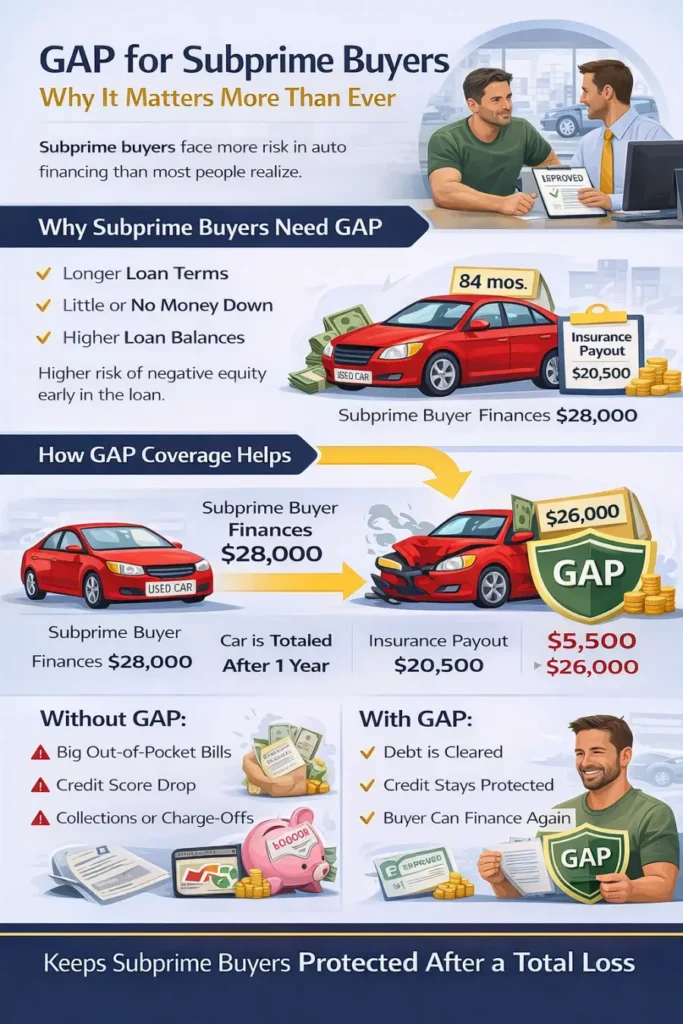

Subprime buyers face more risk in auto financing than most people realize. Longer loan terms, little money down, and higher loan balances make it easier to end up owing more than a vehicle is worth. This is exactly why GAP coverage is especially important for subprime buyers.

When explained clearly, GAP protects buyers from a financial setback that could otherwise damage their credit and limit future buying options.

What Makes a Buyer Subprime

Subprime buyers often:

- Have limited or rebuilding credit

- Finance for 72 months or longer

- Put little or no money down

- Roll negative equity into a loan

These factors increase the chance of negative equity from day one.

Why Subprime Buyers Face Higher GAP Risk

Vehicles lose value quickly. Loan balances for subprime buyers tend to stay higher longer due to:

- Extended loan terms

- Higher interest rates

- Minimal principal reduction early in the loan

If a vehicle is totaled during this period, insurance often pays far less than what is still owed.

How GAP Coverage Protects Subprime Buyers

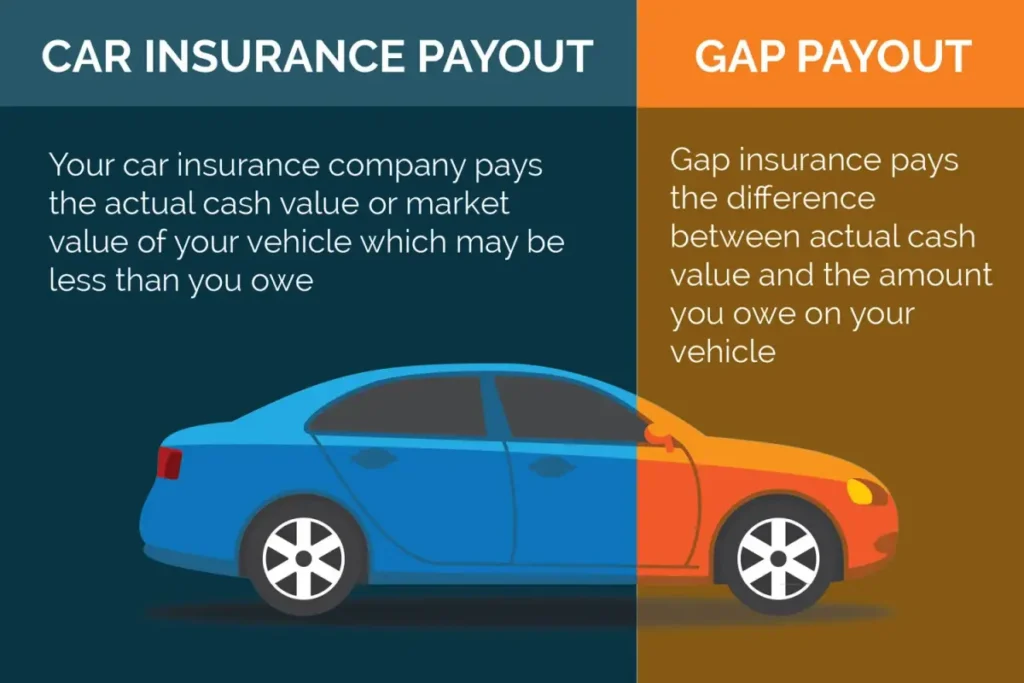

If a vehicle is totaled or stolen:

- Insurance pays market value

- GAP coverage pays the remaining loan balance

This prevents:

- Large out-of-pocket bills

- Collections and charge-offs

- Credit damage during a rebuild period

For subprime buyers, this protection can make the difference between moving forward or falling backward financially.

A Common Subprime GAP Scenario

A buyer finances a used vehicle for $28,000 over 84 months.

After one year, they still owe $26,000.

The vehicle is totaled.

Insurance pays $20,500.

That leaves $5,500 unpaid.

GAP coverage pays that difference.

Without GAP, the buyer is responsible for the balance.

GAP Helps Keep Subprime Buyers in the Market

Without GAP, a total loss can:

- Destroy credit progress

- Prevent future approvals

- Force buyers into higher-risk loans

With GAP:

- The loan is cleared

- Credit stays intact

- The buyer can qualify again

This helps buyers continue improving their financial position.

Why Dealers Should Always Offer GAP to Subprime Buyers

For dealers, GAP coverage:

- Reduces post-sale complaints

- Protects customer relationships

- Prevents charge-offs

- Supports repeat business

Offering GAP is not about pressure. It’s about protection and transparency.

GAP Builds Trust with Credit-Challenged Buyers

Subprime buyers value honesty. When GAP is explained as:

- A safety net

- A way to protect credit

- A smart planning tool

Customers feel informed, not sold.

GAP and Long-Term Financing Go Together

Subprime loans often involve long terms. GAP coverage is designed to work alongside long-term financing by protecting buyers during the highest-risk years of the loan.

This makes GAP a logical part of responsible lending.

Final Thoughts on GAP for Subprime Buyers

GAP coverage protects subprime buyers from one of the biggest risks in auto financing. It helps prevent debt after a total loss and supports long-term credit improvement.

For buyers rebuilding credit and dealers serving them, GAP coverage is not optional protection. It’s practical protection.