When leasing a vehicle, most drivers focus on the monthly payment, mileage limits, and end-of-lease terms. One important protection that often gets overlooked is GAP insurance. Understanding how GAP works for leased vehicles can help prevent unexpected financial stress if the vehicle is totaled or stolen.

This guide explains what GAP insurance is, why it matters for leased cars, and how dealerships and customers benefit from proper GAP coverage.

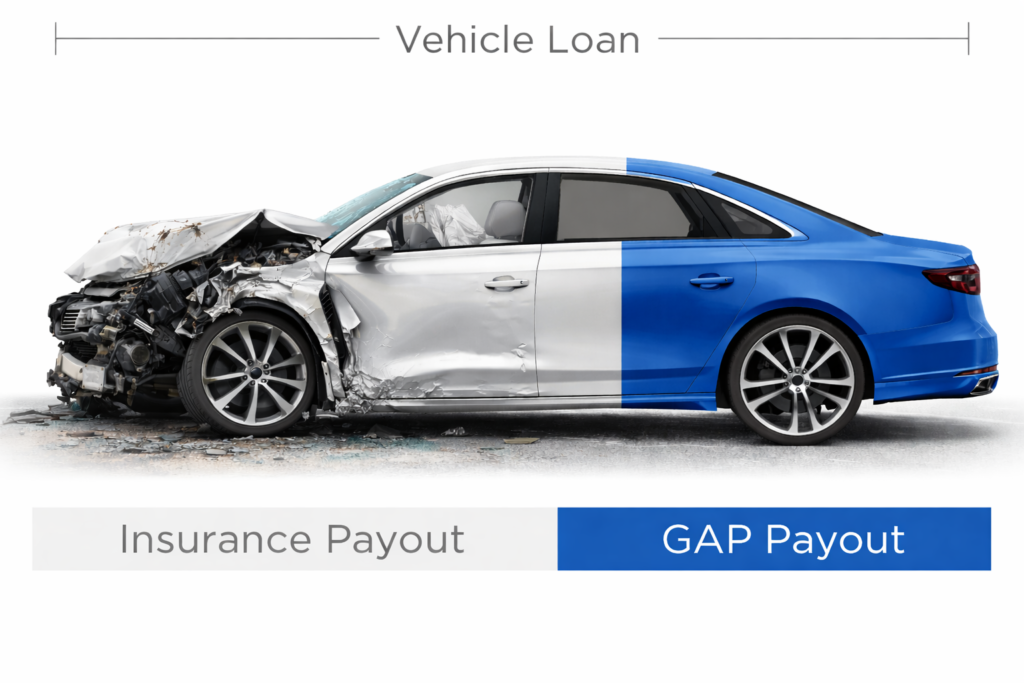

What Is GAP Insurance?

GAP (Guaranteed Asset Protection) helps cover the difference between what an insurance company pays and what is still owed on a vehicle loan or lease after a total loss.

Auto insurance typically pays the actual cash value (ACV) of a vehicle at the time of loss. Because vehicles depreciate quickly, that amount is often less than the remaining balance on a lease.

GAP insurance covers that shortfall, protecting the driver from paying out of pocket for a vehicle they no longer have.

Why GAP Insurance Is Important for Leased Vehicles

Leased vehicles are especially vulnerable to GAP situations for a few reasons:

- Vehicles depreciate quickly during the first years of use

- Lease payoffs are often higher than market value early in the lease

- Down payments on leases are typically low or nonexistent

- Total loss events can happen at any point during the lease term

If a leased vehicle is totaled or stolen, the lessee may still owe thousands of dollars after insurance pays out. GAP insurance steps in to cover that difference.

Does a Lease Include GAP Insurance?

Some lease agreements include GAP coverage, but not all GAP coverage is the same.

Lease-included GAP may:

- Have coverage limits

- Exclude deductible reimbursement

- Offer minimal protection

- Be tied strictly to the leasing company’s terms

In many cases, dealer-offered GAP provides broader coverage, higher limits, and additional benefits such as deductible coverage.

That’s why it’s important for both customers and dealerships to understand what type of GAP is actually in place.

What GAP Insurance Typically Covers on a Lease

While coverage varies by program, GAP insurance for leased vehicles often includes:

- The difference between insurance payout and lease payoff

- Protection in total loss or theft situations

- Coverage during early and mid-lease depreciation periods

- Financial protection that prevents negative lease balance

Some programs may also include deductible coverage, which helps reduce out-of-pocket costs even further.

Common Misunderstandings About GAP on Leases

“My lease already includes GAP, so I don’t need to review it”

Not all GAP coverage is equal. Limits, exclusions, and deductible handling can vary widely.

“GAP only matters if I put no money down”

Even with a down payment, depreciation can still create a GAP situation early in the lease.

“Insurance will take care of everything”

Insurance only pays market value, not what’s owed on the lease.

How GAP Helps Dealerships

From a dealership perspective, GAP insurance provides more than customer protection.

Proper GAP coverage:

- Reduces post-loss customer disputes

- Protects lender relationships

- Improves customer confidence at delivery

- Supports repeat business and referrals

- Adds value to the F&I menu without pressure

For leased vehicles in particular, GAP helps ensure customers leave the dealership fully protected, not exposed to financial surprises.

Expanding GAP Options at the Dealership Level

Some dealerships choose to expand their GAP offering beyond standard programs. This may include:

- Higher LTV limits

- Higher finance caps

- Coverage for specialty vehicles

- Better deductible handling

- Programs that work alongside existing GAP providers

Dealerships don’t always need to replace what they already use. In many cases, adding a GAP option that covers what others don’t creates flexibility and stronger customer outcomes.

GAP Insurance and Customer Confidence

When customers understand how GAP protects them on a lease, it:

- Builds trust

- Reduces anxiety during the buying process

- Prevents frustration after a loss

- Encourages long-term loyalty to the dealership

Clear explanations and the right coverage help customers feel protected rather than sold to.

Final Thoughts

GAP insurance is one of the most important protections for leased vehicles, yet it’s often misunderstood. Whether you’re a customer leasing a car or a dealership reviewing your F&I offerings, understanding how GAP works — and what options are available — makes a real difference.

If you’re a dealership looking to review or expand your GAP coverage limits, exploring additional options can help you protect more customers while strengthening your F&I lineup.

A short conversation can often uncover opportunities to offer better protection without changing what already works.