Long-term auto financing has become the new normal. Loans of 72, 84, and even 96 months are common across both new and used vehicles. While these longer terms help customers afford monthly payments, they also increase financial risk. This is where GAP coverage becomes more important than ever.

Understanding how GAP works with long-term financing helps dealers explain it clearly and helps buyers protect themselves from a situation most don’t expect.

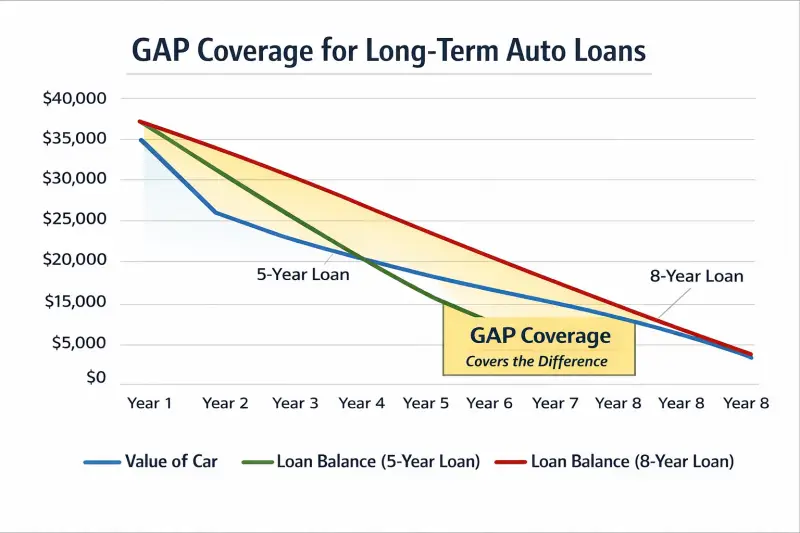

Why Long-Term Loans Create Bigger Risk

Vehicles lose value faster than loans are paid down, especially in the first few years. With longer loan terms:

- Payments reduce the balance more slowly

- Interest adds up over time

- The vehicle’s value drops quickly

This creates a larger gap between what the vehicle is worth and what the customer owes.

The First 24 Months Are the Most Dangerous

The biggest risk period is early in the loan.

During the first one to two years:

- Depreciation is highest

- Loan balances remain high

- Insurance pays market value, not loan balance

If a total loss happens during this time, the gap can be thousands of dollars.

How GAP Coverage Protects Long-Term Loans

GAP coverage steps in when:

- A vehicle is totaled or stolen

- Insurance pays less than the loan balance

GAP pays the difference, helping the customer avoid:

- Large out-of-pocket bills

- Carrying debt on a vehicle they no longer own

- Credit damage

With long-term financing, this protection becomes less optional and more necessary.

Example with an 84-Month Loan

A customer finances a vehicle for $42,000 over 84 months.

After 18 months, they still owe $38,000.

The vehicle is totaled.

Insurance pays $30,500.

That leaves $7,500 unpaid.

GAP coverage covers that difference.

Without GAP, the customer is stuck paying for a vehicle they can’t drive.

Low Monthly Payments Can Be Misleading

Long loan terms make vehicles seem more affordable. But lower payments often mean:

- Less equity

- Longer exposure to depreciation

- More risk if something goes wrong

GAP balances this risk by protecting the loan, not just the vehicle.

Rolling Negative Equity Makes GAP Even More Important

Many buyers roll negative equity from a previous vehicle into a new loan. This pushes the loan balance even higher than the vehicle’s value from day one.

With long-term financing plus negative equity:

- The gap starts immediately

- It lasts longer

- It grows faster

GAP is often the only protection in these situations.

Why Dealers Should Always Present GAP on Long-Term Loans

For dealerships, long-term financing deals are common. Presenting GAP on these deals:

- Helps customers avoid financial stress

- Reduces future complaints

- Protects CSI

- Increases backend profit

When explained properly, GAP feels responsible, not pushy.

GAP Helps Keep Customers in the Market

Without GAP, a total loss can stop a customer from buying again for years. With GAP:

- The loan is cleared

- Credit stays intact

- The customer can replace the vehicle

This keeps customers active and loyal.

GAP Is Built for Today’s Financing Reality

Longer loan terms aren’t going away. Rising prices and tighter budgets make them necessary for many buyers.

GAP coverage is designed to work alongside modern financing, protecting customers from the downside while allowing flexibility on payments.

Final Thought on GAP and Long-Term Financing

Long-term auto loans help customers buy vehicles. GAP coverage helps protect them when things don’t go as planned.

When explained clearly, GAP is one of the most logical and customer-friendly protection products a dealership can offer in today’s financing environment.